Blockchain Technology Explained: Beyond Cryptocurrency

When most people hear the word blockchain, they immediately think of cryptocurrency. While digital currencies helped popularize the technology, they represent only a small part of what blockchain is capable of. That’s why searches for blockchain technology explained have grown; people want to understand the blockchain technology itself, not just coins and trading.

At its core, blockchain is a new way of recording and sharing information securely, transparently, and without relying on a central authority. It introduces a distributed ledger system where data is stored across multiple computers, making it extremely difficult to alter or manipulate. This design has implications far beyond finance, influencing industries such as healthcare, supply chains, digital identity, and governance. This article explains blockchain in simple terms. You’ll learn the blockchain basics, how distributed ledgers work, why blockchain security is considered strong, and how modern web3 technology is building decentralized applications. We’ll also explore real blockchain use cases to show how this Blockchain Technology Explained is already being applied outside cryptocurrency.

What Is Blockchain?

To understand blockchain technology, it helps to strip away the hype and focus on how the system actually works. Blockchain is a method of recording information in a way that makes it transparent, tamper-resistant, and shared across many participants rather than controlled by a single authority.

At the center of blockchain is the distributed ledger. Instead of storing records in one central database, copies of the ledger are maintained across a network of computers (often called nodes). Every participant can verify transactions independently, which reduces the need for trust in a single intermediary. Data on a Blockchain Technology Explained is grouped into blocks. Each block contains a set of transactions, a timestamp, and a cryptographic reference (hash) to the previous block. These blocks are linked together in a chain, which is where the name “blockchain” comes from. If someone tries to alter a record, the hashes break, alerting the network to tampering.

Another core concept is consensus. Because there’s no central controller, the network must agree on which transactions are valid. Consensus mechanisms are rules that nodes follow to validate and add new blocks to the ledger. This agreement process is fundamental to blockchain basics and ensures the integrity of shared data. Finally, blockchain systems emphasize immutability and transparency. Once data is confirmed and added to the chain, it becomes extremely difficult to change. At the same time, transactions are visible to network participants, which increases accountability and auditability, key reasons why blockchain security is considered strong.

How Blockchain Works?

To fully grasp Blockchain Technology Explained technology, it’s important to understand the step-by-step process behind how information moves through a blockchain network. While the blockchain technology may seem complex, the underlying workflow follows a clear and logical structure.

Transactions: Recording Digital Events

Everything on a Blockchain Technology Explained starts with a transaction. A transaction is any digital action that needs to be recorded, such as transferring assets, updating records, or executing a smart contract. Each transaction contains essential details like sender, receiver, timestamp, and data being exchanged. Before being added to the blockchain, transactions are broadcast to the network for verification.

Blocks: Organizing Verified Data

Once transactions are verified, they are grouped into a block. A block acts like a container that holds multiple confirmed transactions along with metadata. Each block includes a cryptographic hash of the previous block, creating a secure link between them. This structure ensures that blocks are added in sequence and prevents unauthorized changes, one of the core blockchain basics.

Consensus: Network Agreement Without Central Control

Because blockchain networks are decentralized, there is no single authority deciding what gets added to the ledger. Instead, the network relies on consensus mechanisms. Consensus is the process through which independent nodes agree that a transaction is valid.

Different blockchains use different consensus methods, but the goal is always the same: to prevent fraud, double-spending, and manipulation while maintaining efficiency. This agreement process is central to maintaining trust and is a key reason behind strong blockchain security.

Immutability Through Cryptography

Once a block is approved and added to the chain, altering it becomes extremely difficult. Changing a single transaction would require modifying every subsequent block and gaining approval from the majority of the network, an impractical task in large systems. This is what gives blockchain its reputation as a tamper-resistant system.

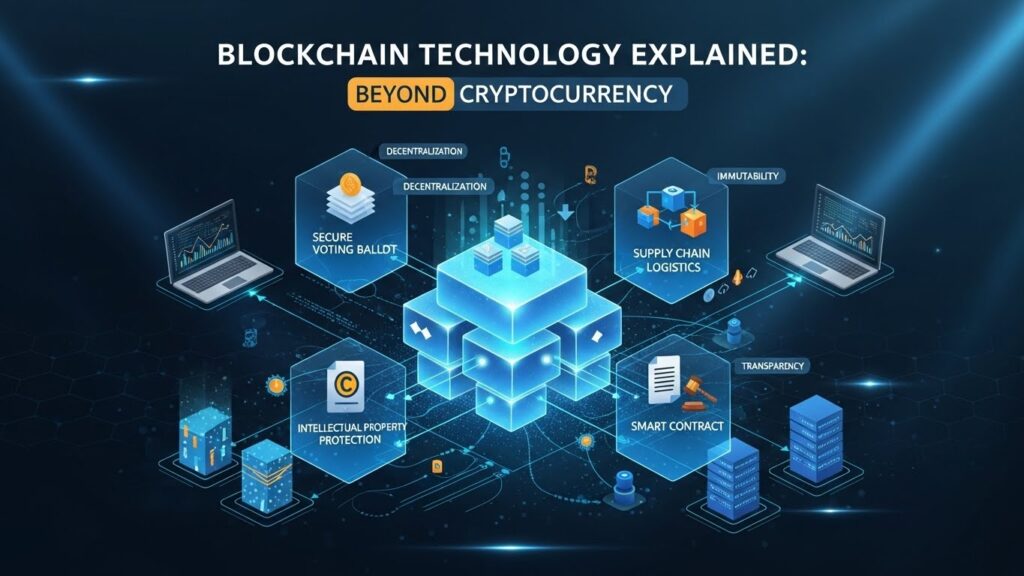

Blockchain Use Cases Beyond Cryptocurrency

While digital currencies brought blockchain into the spotlight, the technology’s real potential lies far beyond financial transactions. Today, organizations across industries are exploring blockchain use cases that leverage transparency, security, and decentralization to solve real-world problems. One major application is supply chain management. Blockchain allows every step of a product’s journey, from raw materials to final delivery, to be recorded on a shared ledger. This improves traceability, reduces fraud, and increases trust between suppliers, manufacturers, and consumers. For industries like food, pharmaceuticals, and luxury goods, this level of visibility is a game-changer.

In healthcare, Blockchain Technology Explained is used to secure and manage patient records. Medical data stored on a distributed ledger can be shared safely between hospitals, doctors, and patients while maintaining privacy and data integrity. This reduces duplication, prevents unauthorized access, and gives patients more control over their information. Digital identity is another growing area. Blockchain-based identity systems allow individuals to verify themselves online without repeatedly sharing sensitive personal details. Instead of relying on centralized databases vulnerable to breaches, identities are validated through cryptographic proofs, enhancing privacy and security. Blockchain also supports smart contracts, which are self-executing agreements written in code. These contracts automatically enforce rules and actions once predefined conditions are met. Smart contracts are widely used in insurance claims, real estate transactions, and automated payments, reducing delays and removing intermediaries.

Conclusion:

Understanding Blockchain Technology Explained helps separate the technology’s real value from the hype around digital currencies. At its core, blockchain introduces a new way to store, verify, and share information using a distributed ledger that removes the need for centralized control. This shift improves transparency, trust, and resilience across digital systems.

As explored through real blockchain use cases, the blockchain technology is already transforming supply chains, healthcare data management, digital identity, and automated agreements. Strong blockchain security, driven by cryptography and consensus, makes records difficult to tamper with, while web3 technology is building decentralized applications that give users greater control over data and assets. Blockchain is not a one-size-fits-all solution, and it comes with challenges around scalability, governance, and adoption. However, when applied thoughtfully, it offers powerful advantages that go far beyond cryptocurrency. Understanding the blockchain basics today provides a solid foundation for evaluating how this blockchain technology will shape digital systems in the years ahead.

FAQs:

1. What does blockchain technology explained mean for beginners?

It means understanding how blockchain records data securely on a shared, tamper-resistant ledger without relying on a central authority.

2. Is blockchain only used for cryptocurrency?

No. Cryptocurrency is just one application. Blockchain is also used in supply chains, healthcare, digital identity, smart contracts, and public records.

3. What is a distributed ledger in blockchain?

A distributed ledger is a database shared across multiple computers, where each participant has a copy that can be independently verified.

4. Why is blockchain considered secure?

Blockchain security comes from cryptography, decentralized validation, and consensus, which make data extremely hard to alter after confirmation.

5. What are common blockchain use cases today?

Common use cases include supply chain tracking, medical records, digital identity verification, smart contracts, and decentralized applications.