Credit Card Minimum Payment Calculator: Free Payoff Tool

With a minimum payment:

Total Interest Paid

Credit Card Minimum Payment Calculator to remind you how “easy” it is to make just the minimum payment each month. It feels safe. It feels affordable. But here’s the uncomfortable truth: sticking to minimums can trap you in debt for decades, costing thousands in interest and leaving your balance almost untouched. What looks like a manageable £50 payment could actually keep you chained to your card until 2040. That’s exactly why we created the FinCalc Credit Card Minimum Payment Calculator. Instead of guessing when you’ll finally be debt-free, our tool shows you the exact payoff timeline, the total interest you’ll pay, and how much faster you can escape debt by making even small changes to your repayment strategy.

Take Sophie, for example. She owed £4,500 on a card at 20% APR. Paying the minimum each month felt manageable, but when she ran the numbers in the Credit Card Minimum Payment Calculator, she discovered it would take more than 17 years to clear, and she’d pay over £8,000 in interest. By committing to £200 per month instead, her debt-free date dropped to just 27 months, saving her nearly £6,500. That single calculation changed the way she approached her finances. The calculator isn’t about complicated formulas or financial jargon. It’s about clarity. Whether you’re juggling one card or several, it turns vague “what-ifs” into clear repayment paths. You don’t have to wonder anymore, you’ll know exactly how long it takes, what it costs, and what you can do today to improve the outcome.

What is a Credit Card Minimum Payment Calculator?

When you open your credit card statement, you’ll usually see two numbers: the total balance you owe, and the minimum payment required for that month. The minimum is often presented as a safety net, a small, “affordable” amount to keep your account in good standing. But what most people don’t realise is that paying only the minimum is one of the slowest and most expensive ways to handle credit card debt.

A Credit Card Minimum Payment Calculator is designed to show you the real cost of following that path. It takes the mystery out of your monthly statement and lays out, in plain numbers, how long it will take to pay off your balance if you only stick to minimum payments, and how much interest you’ll end up paying along the way.

Unlike a generic loan calculator, which assumes fixed monthly payments and simple interest, the Credit Card Minimum Payment Calculator is built specifically for revolving debt. Credit cards come with high APRs, compounding interest, and minimum payments that shrink as your balance decreases. This creates a cycle that looks affordable but stretches repayment timelines for years. Our calculator factors all of this in, so the results reflect reality, not just theory.

Here’s how it works in practice. Let’s say you have:

- A balance of £3,000

- An APR of 20%

- A minimum payment is set at 3% of your balance

At first, that minimum looks manageable, just £90 for the month. But what happens next? Each month, interest is added to the balance, and the minimum payment adjusts downward as the balance falls. The result? Instead of paying off your card in a couple of years, it could take you well over a decade, with thousands of pounds wasted on interest charges. The calculator lays this timeline out clearly, showing you how long you’ll be in debt if you only make the minimum.

At its core, a Credit Card Minimum Payment Calculator isn’t just about math. It’s about giving you visibility. It helps you answer the questions credit card companies don’t want you to ask: How long will this really take? How much will it really cost me? And most importantly, what can I do today to change the outcome? Whether you’re carrying a small balance or juggling several cards, the calculator gives you a roadmap. It strips away the illusion of affordability and replaces it with truth. That truth can be confronting, but it’s also empowering. Because once you know the numbers, you can make smarter choices and finally see a finish line.

Why Minimum Payments Are a Trap

Minimum payments are designed to look harmless. Your credit card statement might say you owe £4,000, but the minimum payment is just £100. Easy enough, right? You pay it, you feel responsible, and you assume you’re making progress. The problem? Most of that money doesn’t even touch your actual balance. It goes straight to covering interest, leaving the principal barely reduced. Month after month, year after year, the balance clings to you like glue. This is the minimum payment trap. It gives you the illusion of affordability while quietly keeping you in debt for years, sometimes decades.

The Illusion of Progress

When you see a balance slowly decreasing, it feels like you’re winning. But with minimum payments, the progress is painfully small. For example, a £5,000 balance at 20% APR with a 3% minimum means your first payment is £150. Sounds fine. But here’s the catch: nearly £83 of that goes to interest, leaving just £67 chipping away at the actual balance. The next month, interest is charged again on a slightly smaller balance, but your minimum payment also shrinks.

The result? Your debt lingers, and the repayment timeline stretches endlessly. The Credit Card Minimum Payment Calculator makes this painfully clear. Instead of vague numbers on a statement, it shows you the full timeline: years of repayment and thousands in extra interest if you stick to minimums.

Interest Piles Up, Not Down

Credit cards are built on compounding interest, meaning you’re charged interest not only on the original balance but also on the interest added each month. That’s why even small balances can spiral out of control. Paying only the minimum keeps compounding alive, ensuring that the lender earns far more from you than the original debt itself. Take a simple scenario:

- Balance: £3,000

- APR: 19%

- Minimum: 2% of balance (£60 first month)

At that rate, it would take more than 14 years to clear, with interest charges exceeding £4,000. That’s right, you’d end up paying more in interest than the debt you originally owed.

The Emotional Toll

The trap isn’t just financial, it’s psychological. Making the minimum can feel like you’re “doing the right thing,” but over time, the lack of progress weighs you down. The statement arrives each month, the balance barely moves, and the frustration builds. Debt that should have been temporary starts to feel permanent, and that sense of hopelessness leads many people to give up or even take on more credit just to cope.

By contrast, when you use the Credit Card Minimum Payment Calculator, you replace that uncertainty with clarity. You see exactly what your current path looks like, and you see how even small adjustments change everything. Suddenly, the balance isn’t a mystery anymore; it’s a plan.

The Banks Know What They’re Doing

It’s important to understand that minimums aren’t an accident; they’re a business model. Banks know that by keeping payments small, customers are less likely to default, but more likely to stay in debt for longer, generating steady interest revenue. It’s no coincidence that card companies highlight minimums in bold while burying the real repayment timeline in fine print. The calculator flips the script. Instead of letting lenders dictate your journey, you take control of it.

Breaking Free from the Trap

The good news is that minimums don’t have to be your reality. The calculator shows how much faster you could be debt-free by paying even slightly more. Adding just £50–£100 extra per month can cut years off your repayment timeline and save thousands in interest. Seeing those savings in black and white is often the motivation people need to break the minimum payment cycle for good.

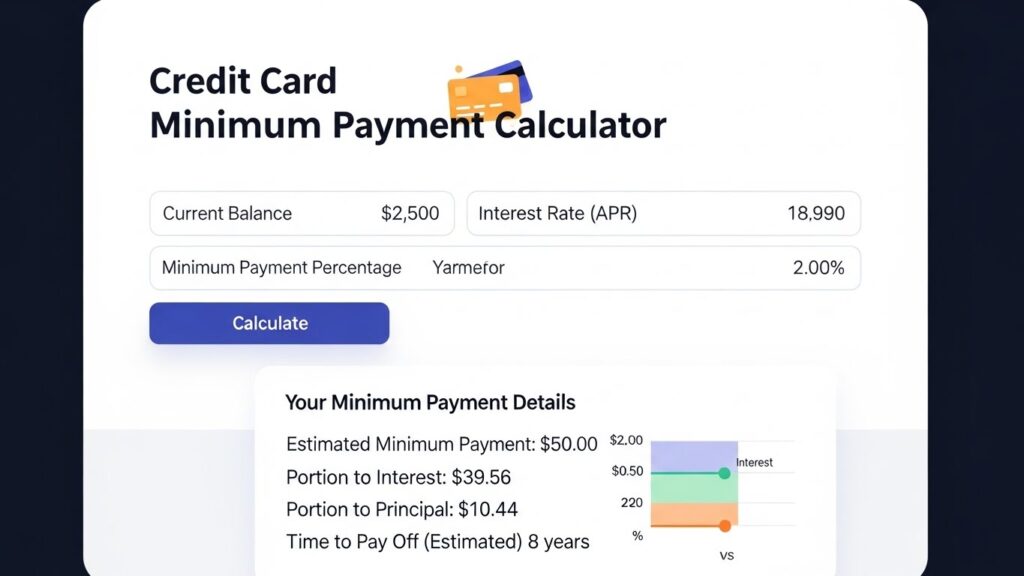

How the Credit Card Minimum Payment Calculator Works

No spreadsheets, no guesswork. In a few inputs, FinCalc’s Credit Card Minimum Payment Calculator shows the true payoff timeline, the total interest you’ll burn, and the quickest levers to get debt-free faster.

Step 1: Enter your balance.

Use your current statement balance (or the balance you plan to tackle first). If you’ve got multiple cards, start with the highest APR, then repeat for the others.

Step 2: Add your APR.

Enter the card’s annual percentage rate. The calculator converts it to a monthly rate and applies compounding just like your issuer.

Step 3: Tell us the minimum rule.

Most cards use “X% of balance or £Y, whichever is higher” (e.g., 3% or £25). Select that rule so the calculator can simulate how the minimum shrinks as the balance falls. Prefer a fixed payment target? Run the same balance in the FinCalc Credit Card Repaymen

t Calculator to lock a monthly amount and see the finish line.

Step 4: Calculate.

You’ll instantly see:

- Time to pay off if you only make the minimum.

- Total interest over the journey.

- A month-by-month view of how each payment splits between interest and principal.

- What-if prompts (e.g., +£25/mo, +£50/mo) with time and interest saved.

Step 5, Iterate.

Toggle from “minimums” to a fixed monthly payment (e.g., £200), or set a target debt-free date and let the tool tell you the monthly amount required. Rinse and repeat until the plan fits your cash flow and your sanity.

Benefits of Using FinCalc’s Credit Card Minimum Payment Calculator

Credit card debt is stressful enough. The last thing you need is confusion about how long repayment will actually take. Yet that’s exactly what happens when you rely on minimum payments and vague statements. The balance never seems to move; the years go on, and interest keeps eating into your paycheck. The FinCalc Credit Card Minimum Payment Calculator is designed to cut through the fog and give you clarity.

1. Clarity Instead of Guesswork

Your statement might show a minimum payment and a due date, but it rarely shows the full journey. Our calculator lays everything out: your debt-free date, total interest, and how small adjustments change the picture. Instead of uncertainty, you finally know the truth.

2. Motivation to Pay More Than the Minimum

It’s hard to stay motivated when your balance barely changes month to month. Seeing that your £3,000 balance could take 14 years to pay off with minimums, versus 24 months with a fixed payment, is often the push people need. The calculator makes progress visible and tangible. To channel extra cash where it saves the most interest, map your plan in the FinCalc Debt Avalanche Calculator and compare months saved.

3. Protects You from the Minimum Payment Trap

Banks design minimums to look affordable, but they keep you paying interest for as long as possible. The calculator shows you how destructive this can be. By making the real cost visible, it protects you from the long-term trap of “just paying the minimum.”

4. Stress-Test Scenarios Without Risk

Want to see how much faster you’ll be debt-free by adding £25, £50, or £100 to your monthly repayment? The calculator runs the numbers instantly. No risk, no commitment, just clear insight into your options.

5. Free, Fast, and Private

No credit checks. No logins. No lender agenda. FinCalc’s tool is completely free and works in seconds. You can run as many scenarios as you like without leaving a mark on your credit report.

FinCalc vs Other Options: The Reality Check

Feature | FinCalc (Minimum Payment Calculator) | Bank Statements | Generic Loan Calculator |

Transparency | Shows timeline, interest, and “what-if” scenarios | Hides long-term cost | Assumes fixed loan, ignores minimums |

Accuracy | Built for credit cards & compounding | Often vague | Misleading for revolving credit |

Flexibility | Test payments, APRs, payoff dates | None | Very limited |

Privacy | 100% free, no login or credit check | Tied to your account | Often requires sign-up |

Real-Life Use Cases of the Credit Card Minimum Payment Calculator

Numbers are powerful, but nothing hits harder than seeing how they play out in real life. Here are some examples of how people from all walks of life use the Credit Card Minimum Payment Calculator to break free from the minimum payment trap.

1. The Graduate Starting Out

Liam just finished university and landed his first job. He carried a balance of £2,500 at 19% APR on his first credit card. He thought paying the £50 minimum was fine until he used the calculator. It revealed that at that rate, it would take over 12 years to clear his balance and cost more than £3,000 in interest. Shocked, Liam tested different payments. By paying £120 a month, he cut his repayment time to 26 months and his interest bill to under £500. The tool turned confusion into a plan.

2. The Family Facing Holiday Debt

James and Laura had a fantastic Christmas but ended up with £8,000 spread across two credit cards at 20% APR. Their bank statements told them the minimums were about £240 combined. Manageable, right? The calculator told a different story: 17+ years of debt and £13,000 in interest if they stuck to minimums. By testing a £400 monthly payment, they saw they could be debt-free in under 3 years, with interest costs slashed to £2,400. For the first time, they felt in control instead of buried. Before changing anything with the bank, they could also price a one-payment option in the Debt Consolidation Calculator to compare total interest side-by-side.

3. The Small Business Owner

Maria ran a design studio and often used her personal credit card to cover business expenses during slow months. Over time, the balance crept to £7,000 at 21% APR. Paying the minimum of about £210 a month felt responsible. But the calculator exposed the truth: it would take more than 20 years to repay, costing nearly £18,000 total. By increasing her monthly payment to £350, the calculator showed she’d be debt-free in 29 months, saving over £9,000 in interest. Seeing the numbers helped her adjust her budget and negotiate smarter with suppliers.

4. The Gadget Enthusiast

Daniel loved upgrading his tech, new phones, laptops, and gaming gear. His balance climbed to £4,000 at 20% APR. He figured paying £100 a month kept things under control. The calculator shattered that illusion: his balance would take 15 years to clear, with more than £6,500 in interest. Testing a fixed payment of £220, Daniel saw he could be debt-free in less than 2 years, with under £900 interest. That reality check made him rethink impulse upgrades and focus on repayment.

5. The Retiree on a Fixed Income

Eleanor was retired and living on a modest pension. She had a £3,200 balance at 18% APR. Her card company’s minimum payment of about £70 looked doable, but the calculator revealed a 13-year timeline and over £3,500 in interest. She tested a £150 monthly repayment and saw she could be free in 25 months, saving almost £2,400. For Eleanor, the tool didn’t just show numbers; it gave her peace of mind.

Conclusion

Credit card debt often feels like quicksand. Every month, you make the minimum payment, but the balance barely moves. Interest keeps piling on, and what started as a manageable expense turns into years, sometimes decades, of financial stress. The truth is simple: minimum payments are designed to keep you stuck. They give you the illusion of progress while quietly draining your money through interest charges. This is why the Credit Card Minimum Payment Calculator exists. It cuts through the confusion and exposes the real cost of paying only the minimum. With just a few quick inputs, you see the full picture: how many years it will actually take to pay off your balance, how much interest you’ll throw away, and how much faster you could be debt-free by increasing your payments even slightly. Instead of vague guesses, you get hard facts, numbers that empower you to take action.

Imagine the difference. One person keeps paying the £60 minimum on a £3,000 balance at 19% APR, trapped in debt for more than a decade and paying over £4,000 in interest. Another person, armed with the calculator, sees that by raising their payment to £150 a month, they’ll be free in just over two years and save thousands. The debt hasn’t changed, but the plan has, and that’s the power of knowledge. But this isn’t just about numbers. It’s about peace of mind. It’s about seeing the finish line and knowing you’re not throwing away your future income on endless interest. It’s about replacing stress and uncertainty with clarity and control. Whether you’re a student managing your first card, a family juggling multiple balances, a retiree on a fixed income, or a business owner using personal credit for cash flow, the calculator adapts to your situation and gives you the roadmap you need. And unlike bank statements or generic calculators, FinCalc’s Credit Card Minimum Payment Calculator is built for real life. It’s independent, free, and completely private. No sign-ups. No hidden agendas. No credit checks. Just an honest picture of where you stand and how to change it.

Frequently Asked Questions (FAQ)

What is a Credit Card Minimum Payment Calculator?

A Credit Card Minimum Payment Calculator is a tool that shows you how long it will take to clear your balance if you only make the minimum payments. By entering your balance, APR, and minimum payment rule, the calculator estimates your payoff timeline and the total interest you’ll pay. It’s designed to reveal the hidden cost of minimum payments, which often stretch repayment across 10–20 years. With this tool, you see the reality in seconds and can test how paying more changes everything.

Why are minimum payments dangerous?

Minimum payments look affordable, but they’re designed to keep you in debt for as long as possible. Most of your payment goes toward interest, with only a small portion reducing the balance. For example, on a £5,000 balance at 20% APR, your minimum might be £150, but around £80 of that is just interest. The Credit Card Minimum Payment Calculator shows you how little progress minimum make and why paying more each month saves years and thousands in interest.

How accurate is the Credit Card Minimum Payment Calculator?

The calculator uses the same formulas card issuers apply: APR converted to monthly interest, compounding, and minimum payment rules like “3% or £25.” While exact numbers can vary slightly between lenders (daily vs monthly compounding, fees), the results are very close to real repayment outcomes. It’s one of the most reliable ways to forecast your debt-free date and interest cost before you make a repayment plan.

Can the calculator work for multiple credit cards?

Yes. You can run the Credit Card Minimum Payment Calculator for each card individually, then add the totals for a full picture. Many people use it alongside repayment strategies like the debt snowball (paying off the smallest balance first) or the avalanche method (targeting the highest APR first). By seeing how long each card would take with minimums, you can decide which one to prioritise and how extra payments will save the most money.

Does the calculator show total interest?

Absolutely. One of its key features is breaking down how much of your repayment goes to interest versus the balance. This is eye-opening for most people because it highlights why minimum payments are so expensive in the long run. For example, a £3,000 balance at 19% APR could cost over £4,000 in interest with minimum payments, but under £700 with fixed payments. The calculator makes these savings clear.

Can I see what happens if I pay more than the minimum?

Yes. That’s the main benefit. The Credit Card Minimum Payment Calculator lets you test different payment amounts instantly. You can enter your balance and APR, then compare scenarios: minimums, fixed monthly payments, or even setting a target debt-free date. The results show how much faster you’ll be debt-free and how much interest you’ll save by paying a little extra.