Compound Interest Calculator: Compare Simple vs Compound Growth

Understanding how interest works is crucial for making smart financial decisions, whether you are saving, investing, or borrowing money. Two common types of interest, simple interest and compound interest, can lead to very different outcomes over time. While simple interest calculates growth only on your initial investment or loan, compound interest allows your money to grow exponentially by earning “interest on interest.”

The difference might seem small at first, but over months and years, it can have a huge impact on your savings or debt. A Compound Interest Calculator can help you clearly see how your money grows under both scenarios, making it easier to plan and optimise your financial strategy. In this guide, we’ll explain what simple and compound interest are, highlight their key differences, provide practical examples, and show how to use a Compound Interest Calculator to make informed financial decisions.

What Is Simple Interest?

Simple interest is a method of calculating interest where the interest is applied only to the original principal amount of a loan or investment. It does not take into account any interest that has already been earned or charged, making the growth linear rather than exponential.

The formula for simple interest is:

SI=P×r×tSI = P \times r \times tSI=P×r×t

Where:

- SISISI = simple interest

- PPP = principal amount

- rrr = annual interest rate (in decimal)

- ttt = time in years

Example:

If you invest £1,000 at a 5% annual simple interest rate for 3 years:

- Interest earned = £1,000 × 0.05 × 3 = £150

- Total balance after 3 years = £1,150

Simple interest is commonly used in short-term loans, personal loans, or certain fixed deposits, where the principal remains constant and the interest is predictable. While it’s easy to calculate and understand, it does not leverage the power of compounding, which means your money grows more slowly compared to compound interest.

What Is Compound Interest?

Compound interest is the method of calculating interest on both the initial principal and the accumulated interest from previous periods. This “interest on interest” effect allows your money to grow exponentially over time, making it much more powerful than simple interest for long-term savings and investments.

The basic formula for compound interest is:

A=P×(1+rn)n×tA = P \times \left(1 + \frac{r}{n}\right)^{n \times t}A=P×(1+nr)n×t

Where:

- AAA = the future value of your investment or loan

- PPP = principal amount

- rrr = annual interest rate (in decimal form)

- nnn = number of times interest is compounded per year

- ttt = number of years the money is invested or borrowed

Example:

If you invest £1,000 at a 5% annual interest rate, compounded annually, for 3 years:

- Year 1: £1,000 × 1.05 = £1,050

- Year 2: £1,050 × 1.05 = £1,102.50

- Year 3: £1,102.50 × 1.05 = £1,157.63

Compound interest is widely used for savings accounts, retirement funds, and long-term investments because it significantly increases wealth over time, especially when combined with regular contributions and higher compounding frequencies.

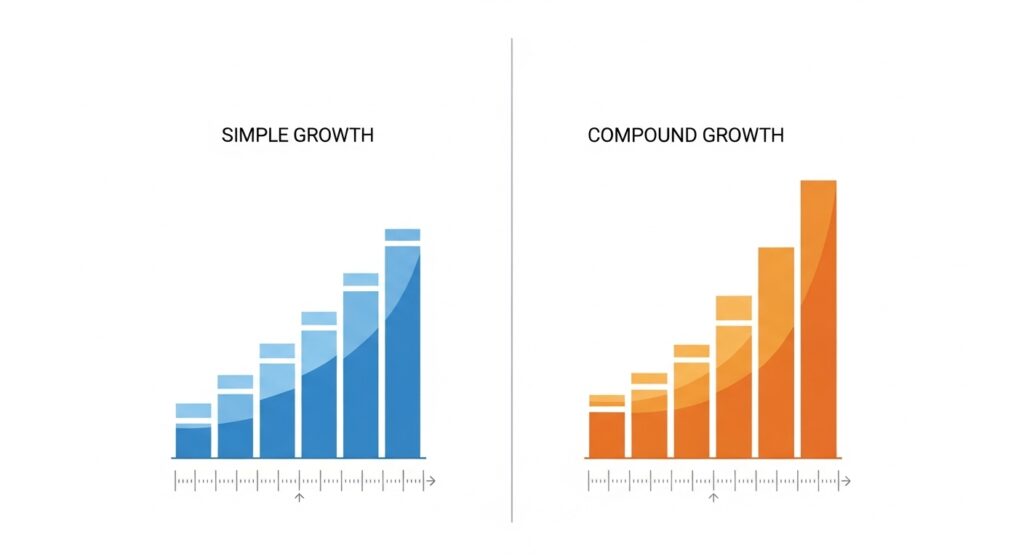

Key Differences Between Simple and Compound Interest

Visit Fincalc.uk. Understanding the differences between simple and compound interest is essential for making informed financial decisions. Here’s a breakdown of the key distinctions:

Aspect | Simple Interest | Compound Interest |

Calculation Method | Interest is calculated only on the principal amount. | Interest is calculated on the principal plus accumulated interest. |

Growth Over Time | Linear growth; the same amount of interest is earned each period. | Exponential growth; interest grows faster as it compounds over time. |

Effect of Time | Longer periods increase interest, but growth is predictable and steady. | Longer periods dramatically increase total returns due to compounding. |

Ideal Use Cases | Short-term loans, personal loans, and simple fixed deposits. | Long-term savings, retirement accounts, and investments. |

Complexity | Easy to calculate and understand. | More complex, but tools like a Compound Interest Calculator simplify the process. |

Using a Compound Interest Calculator to Compare

A Compound Interest Calculator is an excellent tool for visualising the difference between simple and compound interest. Instead of manually calculating both methods, you can enter the principal amount, interest rate, time period, and compounding frequency to see how your money grows under each scenario. For example, investing £1,000 at a 5% annual interest rate for 10 years:

- Simple interest would give you £1,500 total.

- Compound interest (compounded annually) would grow to approximately £1,629.

Using the calculator, you can experiment with different contribution amounts, time periods, and compounding frequencies to see how they impact your savings or investment growth. This makes it easier to plan for goals such as building an emergency fund, saving for a house, or preparing for retirement. By visually comparing simple versus compound interest, a Compound Interest Calculator helps you understand the long-term benefits of compounding and make smarter financial decisions.

Conclusion:

Understanding the difference between simple interest and compound interest is essential for making informed financial decisions. While simple interest provides predictable, linear growth, compound interest has the potential to significantly accelerate wealth accumulation over time due to its “interest on interest” effect.

Using a Compound Interest Calculator makes it easy to compare both methods and see the real impact of compounding on your savings, investments, or even loans. Practical examples show that starting early, contributing consistently, and allowing interest to compound can make a dramatic difference in achieving financial goals such as retirement, buying a home, or building an emergency fund. By mastering the concept of compound interest and leveraging it effectively, you can make smarter financial choices, maximise growth, and take control of your financial future.

FAQs:

1. Can simple interest ever outperform compound interest?

In most long-term scenarios, compound interest will always outperform simple interest because it earns interest on both principal and accumulated interest. Simple interest may only be better for very short-term loans or deposits.

2. How much does compounding frequency matter?

The more frequently interest compounds (daily, monthly, quarterly), the faster your money grows. Monthly or daily compounding typically yields higher returns than annual compounding.

3. Can compound interest work against me with loans?

Yes. On loans like credit cards, compound interest increases what you owe over time. Understanding the difference helps you avoid costly debt accumulation.

4. How do I calculate compound interest easily?

Using a Compound Interest Calculator simplifies the process. You input the principal, interest rate, time, and compounding frequency to see projected growth instantly.

5. Why is starting early important?

The earlier you start saving or investing, the longer your money has to compound, which significantly increases total growth over time.