How does an NI Contributions Calculator Help You Balance Pay and Pensions?

When you look at your payslip, it can sometimes feel like a puzzle; your gross salary rarely matches the amount you actually take home. That’s because several deductions are made before your net pay reaches your bank account. Among the most important are National Insurance (NI) contributions and pension contributions, both of which play a big role in shaping your current finances and your future security. National Insurance contributions help fund essential state benefits such as the NHS, unemployment support, and the state NI Contributions Calculator Help pension, making them a mandatory part of working in the UK. Pension contributions, on the other hand, are usually linked to your workplace or personal pension scheme and represent your investment in retirement savings. While both reduce your take-home pay today, they serve very different purposes in the long run.

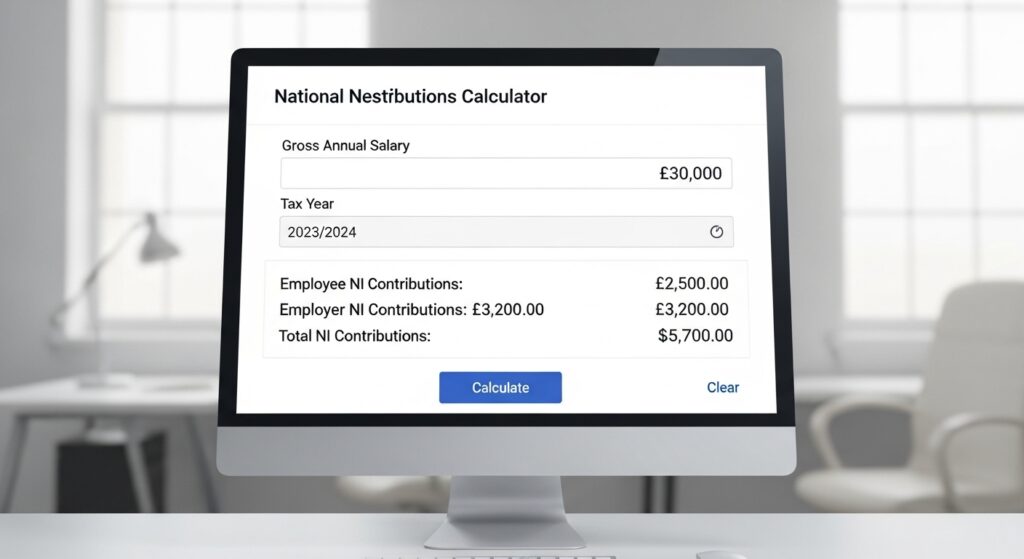

To better understand how these deductions affect your salary, tools like an NI Contributions Calculator can be invaluable. By clearly breaking down your NI payments, these calculators give you transparency over your earnings and help you make smarter financial decisions, especially when balancing day-to-day expenses with future savings. In this article, we’ll explore the differences between NI contributions and pension contributions, how they both impact your salary, and why understanding them is key to effective financial planning.

What Are National Insurance Contributions?

National Insurance contributions, often shortened to NI contributions, are mandatory payments made by employees, employers, and self-employed individuals in the UK. They are separate from income tax and are specifically designed to fund NI Contributions Calculator Help key elements of the country’s social security system. This includes the state pension, the National Health Service (NHS), unemployment benefits, maternity allowance, and support for people who are sick or disabled. For employees, NI contributions are automatically deducted from wages through the Pay As You Earn (PAYE) system. Employers also contribute on top of what employees pay, helping to maintain a balanced system. Self-employed individuals, meanwhile, are responsible for paying their contributions directly, usually through their annual tax return.

There are several types of NI contributions, known as “classes.” Class 1 contributions are paid by employees and employers, based on earnings above a certain threshold. Class 2 contributions are a flat weekly rate for the self-employed, while Class 4 contributions are calculated as a percentage of annual profits. Understanding which class applies to you is crucial, as it affects both how much you pay and which benefits you are entitled to later. Because NI contributions can be complex, many people turn to an NI Contributions Calculator. This tool quickly calculates your likely payments based on your income and employment status, providing a clear picture of how much you are contributing and the impact it has on your take-home salary.

What Are Pension Contributions?

Pension contributions are regular payments made into a retirement savings scheme, usually deducted directly from your salary. Unlike National Insurance contributions, which are mandatory and fund state benefits, pension NI Contributions Calculator Help are primarily designed to build your personal retirement pot. In most cases, employees are automatically enrolled into a workplace pension scheme, with contributions made by both the employee and their employer. The government also supports these savings by offering tax relief, which means a portion of the money that would have gone to tax instead goes into your pension. There are different types of pension schemes. Workplace pensions are the most common, where both you and your employer contribute. Some employers offer to match or even exceed your contributions, making it a valuable benefit. Personal pensions are another option, allowing individuals to save for retirement independently, often with more investment choices. Auto-enrolment rules introduced in the UK mean that most eligible employees are now automatically added to a workplace scheme, although you can choose to opt out.

The way contributions are deducted can also vary depending on the scheme. Some pension contributions are taken out of your gross pay before tax, reducing the amount of tax you owe. Others are deducted after tax, with tax relief added back by the provider. Either way, these payments represent a long-term investment in your financial security, ensuring you have income to rely on once you retire. Although pension contributions reduce your take-home pay today, they can make a significant difference in the future. That’s why it’s important to strike a balance, contributing enough to grow your retirement savings without straining your current finances. Just as you might use an NI Contributions Calculator to understand your NI payments, pension calculators are useful tools to project how today’s contributions will benefit you in retirement.

NI Calculator vs Pension Contributions: Key Differences

While both National Insurance contributions and pension contributions appear as deductions on your payslip, they serve very different purposes. National Insurance contributions are mandatory payments that go directly to the government to fund essential services such as the NHS, unemployment support, and the state pension. You don’t get to NI Contributions Calculator Help choose how much you contribute, as the rates and thresholds are set by HMRC. An NI Contributions Calculator can show you exactly how much is deducted from your salary based on your earnings, but you cannot alter the obligation itself.

Pension contributions, on the other hand, are largely about personal choice and long-term savings. While auto-enrolment means most employees are automatically added to a workplace pension scheme, you do have flexibility to increase, decrease, or even opt out of contributions (though opting out means losing valuable employer contributions and tax relief). These payments don’t fund public benefits; instead, they build a private pot of money that you will use in retirement.

Conclusion

Both National Insurance contributions and pension contributions directly affect your salary, but they do so in very different ways. NI Contributions Calculator Help are mandatory and ensure you remain eligible for vital state benefits, such as the NHS and the state pension, while pension contributions represent your personal investment in retirement security. Together, they shape both your present take-home pay and your future financial stability.

Using an NI Contributions Calculator can help you clearly see how much of your income is allocated to NI, while pension calculators allow you to project how today’s contributions will grow into tomorrow’s retirement savings. By understanding both, you can make informed financial decisions, balancing the need to manage current expenses with the importance of preparing for life after work. Ultimately, knowing the difference between these two deductions and how they interact on your payslip puts you in control of your money, helping you plan smarter for both the short term and the long term.

FAQs

Do I have to pay both National Insurance and pension contributions?

Yes, if you are employed, the NI contributions calculator is mandatory and deducted automatically, while pension contributions are usually made through auto-enrolment schemes. You can opt out of pension contributions, but NI must be paid if your earnings are above the threshold.

Can I reduce my National Insurance contributions?

No, NI contributions are set by the government and cannot be reduced. However, using an NI Contributions Calculator helps you estimate exactly what you’ll pay so you can plan your budget.

How do pension contributions affect my salary?

Pension contributions reduce your take-home pay today, but they are invested in your retirement fund. In many cases, contributions also benefit from tax relief and employer top-ups, making them highly valuable for long-term financial security.

Does paying more into my pension reduce my NI contributions?

No, NI contributions are based on your gross earnings above certain thresholds and are unaffected by how much you contribute to your pension. However, higher pension contributions can reduce your taxable income, which may lower your income tax bill.